Switch mortgage lender Australia: How to Beat the 2026 Bank 'Loyalty Tax' and Save Thousands

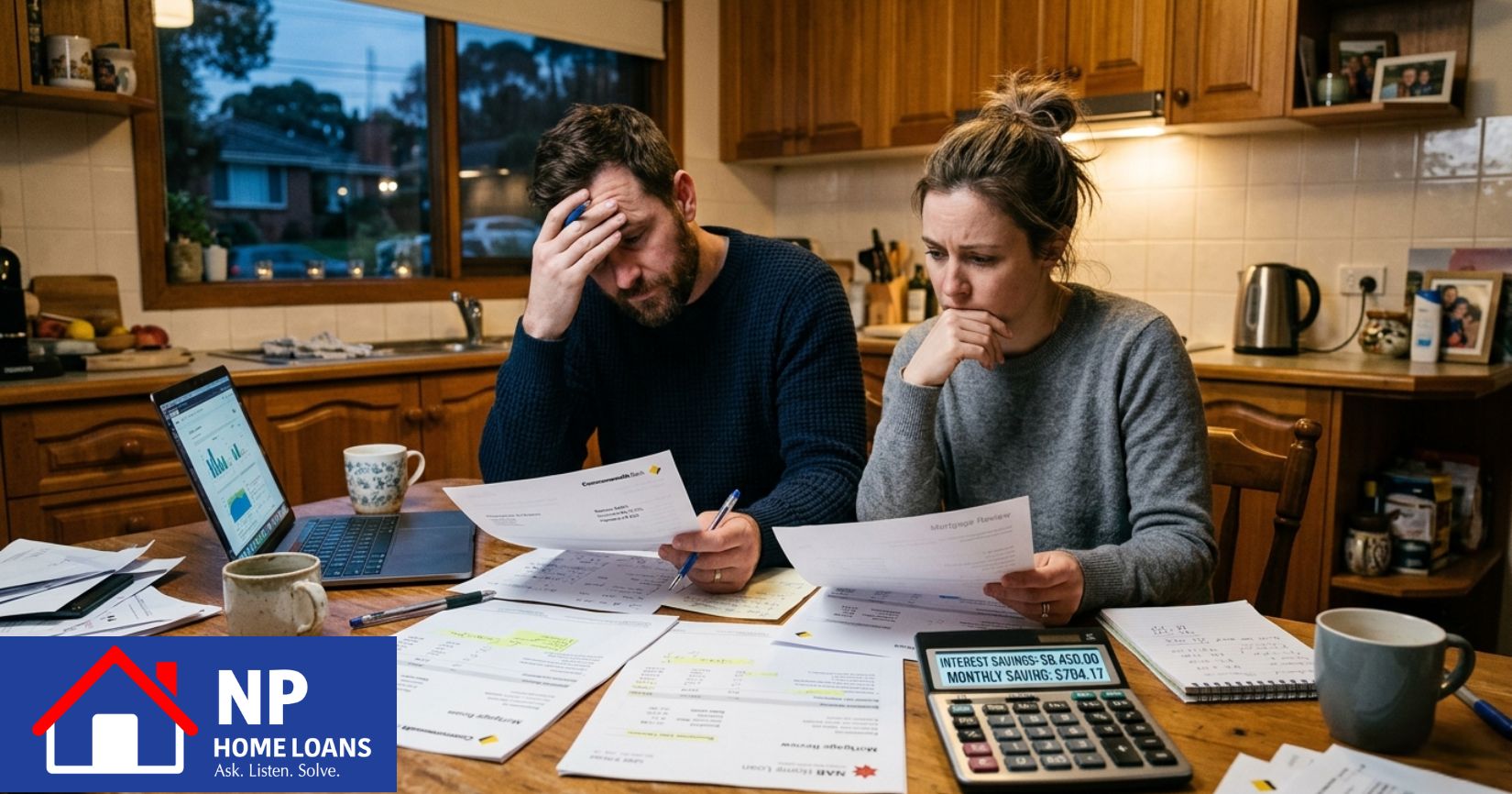

If you have been keeping an eye on your bank statements lately, you do not need an economist to tell you that the financial ground is shifting. With the Reserve Bank of Australia lifting the cash rate to 4.10% following persistent inflation pressures, mortgage stress across Melbourne’s south-east is hitting kitchen tables hard.

From the leafy streets of Mt Waverley to the family hubs of Chadstone and Monash, everyday homeowners are watching their hard-earned money disappear into extra interest payments.

But here is the inside secret that the big banks do not want you to know: if you have been with the same lender for more than two years, you are almost certainly paying a mortgage loyalty tax. Banks routinely offer their lowest, most competitive rates to win over new customers, while quietly keeping their existing, loyal clients on much higher variable rates.

If you are wondering how to switch mortgage lender Australia safely without getting trapped by hidden fees, this guide will show you exactly how to take back control of your cash flow.

Why Staying 'Loyal' to Your Bank Is Costing You

Most people think refinancing is too much of a headache. They look at the paperwork, assume the savings are minimal, and put it off for another six months. This procrastination is exactly what major lenders count on.

Let’s look at the actual numbers. If you have an outstanding loan balance of $750,000—which is very common for properties around Chadstone and Monash—even a tiny interest rate difference of 0.50% translates to roughly $3,750 a year in pure waste. That is money that could go toward your kids’ school fees, groceries, or gas bills.

When you decide to switch mortgage lender Australia, you aren’t just chasing a lower number. You are actively choosing to stop overpaying for a product that does the exact same job elsewhere.

Best Practices When Preparing to Switch Lenders

Audit Your Current Setup: Know your current interest rate, your remaining loan term, and whether you have a fixed or variable setup. If you are on a fixed rate, check if there are break costs involved.

Look Beyond the Headline Rate: A super-low rate looks great on a billboard near Chadstone Shopping Centre, but what are the ongoing account fees? Does the new loan include a fully functional offset account or free redraw facilities?

Calculate the Break-Even Point: Switching lenders does come with small upfront costs, like discharge fees from your current bank and application fees for the new one (usually totaling around $600 to $1,000). Your savings should easily outpace these costs within the first few months

Actionable Tips to Break Out of 'Mortgage Prison'

With stricter lending criteria in 2026, some homeowners worry they are stuck in “mortgage prison”—meaning they want to switch but fear their borrowing capacity has dropped too much to get approved elsewhere.

Here is how we handle this at NP Home Loans to ensure you secure a win:

| Step | Focus Area | What to Do |

| 1 | Clean Up Daily Spending | For three months before applying, minimize discretionary spending and eliminate unused subscriptions. Lenders scrutinize living expenses closely. |

| 2 | Reduce Credit Limits | A $10,000 credit card limit reduces your borrowing capacity by roughly $50,000, even if the card balance is zero. Close or reduce unused cards. |

| 3 | Use a Local Expert | Instead of guessing which bank will accept your application, let a specialized mortgage broker Monash expert map your financial profile against 30+ lenders simultaneously. |

By working with an independent broker who knows the Mt Waverley and Chadstone property landscapes, you do not have to guess which bank will look favorably on your situation. We do the heavy lifting for you.

Frequently Asked Questions (FAQ)

Q1: How long does it take to switch mortgage lenders in Australia?

A: Typically, the entire process takes between 2 to 4 weeks from your initial application to settlement. This includes your new lender evaluating your property and your old lender processing the discharge forms.

Q2: Can I switch lenders if my property value has dropped?

A: Yes, but it depends on your remaining equity. If your loan-to-value ratio (LVR) goes above 80% due to market shifts, you might have to pay Lenders Mortgage Insurance (LMI). A professional home loan health check mt waverley can help calculate whether switching is still financially viable for you.

Q3: Is it worth switching lenders for a 0.5% lower rate?

A: Absolutely. On a typical Melbourne mortgage of $700,000, a 0.5% reduction in your interest rate can save you over $200 every single month. Over a few short years, that adds up to ten thousand dollars kept in your pocket instead of the bank’s vault.