Best Mortgage Options for Sole Traders in Australia

Running your own business across Mt Waverley, Chadstone, or the broader Monash area is incredibly rewarding, but it comes with a unique set of challenges. When it’s time to stop renting or upgrade the family home, many self-employed professionals face a frustrating brick wall.

You walk into a traditional bank, stack of inconsistent bank statements in hand, only to feel judged by a rigid system built for 9-to-5 PAYG employees. The real pain isn’t just the paperwork; it’s the underlying anxiety that your hard work won’t be recognized because your tax accountant did a fantastic job legally minimizing your taxable income.

The good news? You do not need a standard payslip to secure your dream property. Australia’s mortgage landscape offers highly flexible pathways specifically designed for your business structure. Let’s break down the best mortgage options for sole traders in Australia and exactly how to position your application for a guaranteed win.

1. The Full Doc Self-Employed Loan

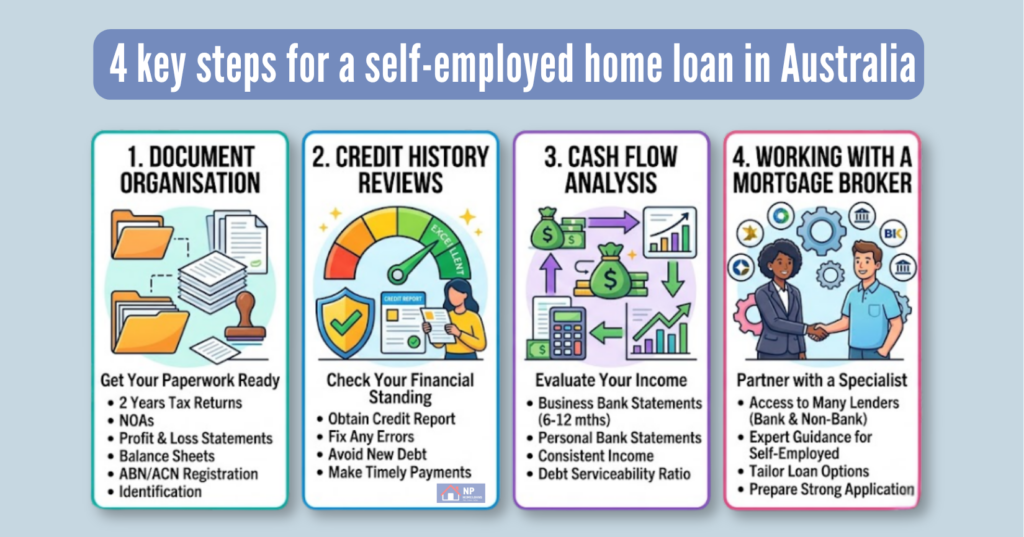

If your books are entirely up to date and you have been operating with an active Australian Business Number (ABN) for over two years, a Full Doc (Full Documentation) Home Loan is usually your cheapest path forward.

Mainstream lenders will assess your financial stability using your official tax declarations. For a sole trader, this means they will look directly at your personal tax returns and your official Australian Taxation Office (ATO) Notices of Assessment (NOA).

The Catch: Lenders typically average your net profit over the last two financial years. If your income spiked recently or fluctuated due to seasonal shifts, traditional banks might calculate your borrowing power based on your lowest-earning year.

The NP Advantage: We work with specific lenders who are willing to evaluate your application based purely on your most recent year of trading if the business shows upward momentum.

2. Low Doc and Alt Doc Home Loans

What happens if your latest tax returns aren’t finalized, or your net profit looks low on paper due to smart asset write-offs? This is where Low Doc (Low Documentation) or Alt Doc (Alternative Documentation) home loans become a complete lifesaver.

These loans are explicitly designed for small business owners who are highly profitable but do not fit into a standard banking box. Instead of demanding two years of tax returns, an alt doc loan allows you to verify your business income using alternative evidence:

Business Activity Statements (BAS): Typically, showing your last 6 to 12 months of BAS is enough to prove stable cash flow.

Business Bank Statements: Supplying 3 to 6 months of active business bank statements to demonstrate consistent trading income.

Accountant’s Declaration Letter: A formal letter signed by a qualified accountant confirming your business’s financial viability and regular earnings.

While alt doc loans sometimes carry a slightly higher interest rate or require a larger deposit (usually a 20% deposit to avoid Lenders Mortgage Insurance), they provide immediate market access without waiting for tax seasons to close.

Best Practices & Actionable Tips for Local Sole Traders

To jump to the front of the queue and secure an elite interest rate, follow these core steps before putting a deposit down on a property in Chadstone or Mt Waverley:

Keep Finances Strictly Separate: Never mix your personal grocery bills with your business expenses. Clean, separate bank accounts show lenders that you run a disciplined operation.

Understand ‘Add-Backs’: Experienced mortgage brokers can add one-off expenses back into your paper profit to boost your borrowing capacity. This includes things like large instant asset write-offs, depreciation on vehicles, or voluntary superannuation contributions.

Boost Your Credit Score: Pay down credit card limits and close unused overdraft facilities. Lenders evaluate your total available credit limits as if they are fully maxed out, which directly chokes your borrowing capacity.

Frequently Asked Questions

Q1: Can I get a sole trader home loan if I’ve been trading for less than 2 years?

A: Yes. While traditional major banks heavily prefer a 2-year ABN history, specialist lenders will consider your application with a 12-month ABN (or even 6 months in select scenarios) if you have extensive prior experience working in the exact same industry.

Q2: Do low doc loans require a higher interest rate?

A: Not always. If you have a strong 20% deposit and immaculate repayment histories on your existing liabilities, many non-bank lenders offer alt doc rates that sit incredibly close to standard mainstream product rates.

Q3: How do lenders calculate income for a sole trader?

A: Unlike a company structure where profits can sit inside a corporate entity, all net profit generated by a sole trader belongs to the individual. Lenders take your gross business revenue, subtract your legitimate business operating expenses, and utilize that net figure as your primary servicing income.